1. What is the Asia Pacific Seaweed Derivatives Market Overview – definition, scope, and significance?

The Asia Pacific Seaweed Derivatives Market encompasses the production, processing, and distribution of functional ingredients extracted from marine seaweeds, including liquids, powders, and flakes. These derivatives are sourced from red, brown, and green seaweed species and serve multiple end‑use sectors such as food and beverages, agricultural products, animal feed additives, and pharmaceuticals. The market’s significance lies in its contribution to sustainable bioproducts, growing consumer demand for natural additives, and the region’s abundant coastal resources that position Asia Pacific as a global hub for seaweed cultivation and innovation.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Seaweed Derivatives Market?

Key drivers include rising health‑consciousness, increasing demand for clean‑label ingredients, and governmental support for marine biotechnology. Restraints stem from limited processing infrastructure in some coastal countries and price sensitivity in bulk applications. Challenges involve stringent regulatory requirements for food‑grade derivatives and competition from synthetic alternatives. Opportunities arise from expanding applications in nutraceuticals, bio‑fertilizers, and marine‑based pharmaceuticals, as well as advancements in extraction technologies that improve yield and functionality.

3. What growth trends are currently influencing the Asia Pacific Seaweed Derivatives Market?

Current trends feature a shift toward high‑purity liquid extracts for functional beverages, the adoption of powdered seaweed as a protein‑rich additive in plant‑based foods, and the growing popularity of seaweed flakes as natural flavor enhancers. Emerging trends include the integration of seaweed derivatives into biodegradable packaging, the use of brown‑seaweed alginates in controlled‑release drug formulations, and collaborative research programs between universities and industry to develop novel green‑seaweed bioactives.

4. How has COVID‑19 impacted the Asia Pacific Seaweed Derivatives Market, and what is the recovery outlook?

The pandemic initially disrupted supply chains due to lockdowns in major producing countries, leading to temporary inventory shortages. However, heightened awareness of immunity‑boosting foods accelerated demand for seaweed‑based functional ingredients. Recovery has been strong, with production volumes rebounding in 2022 and a clear upward trajectory driven by post‑pandemic consumer preferences for natural, health‑supporting products.

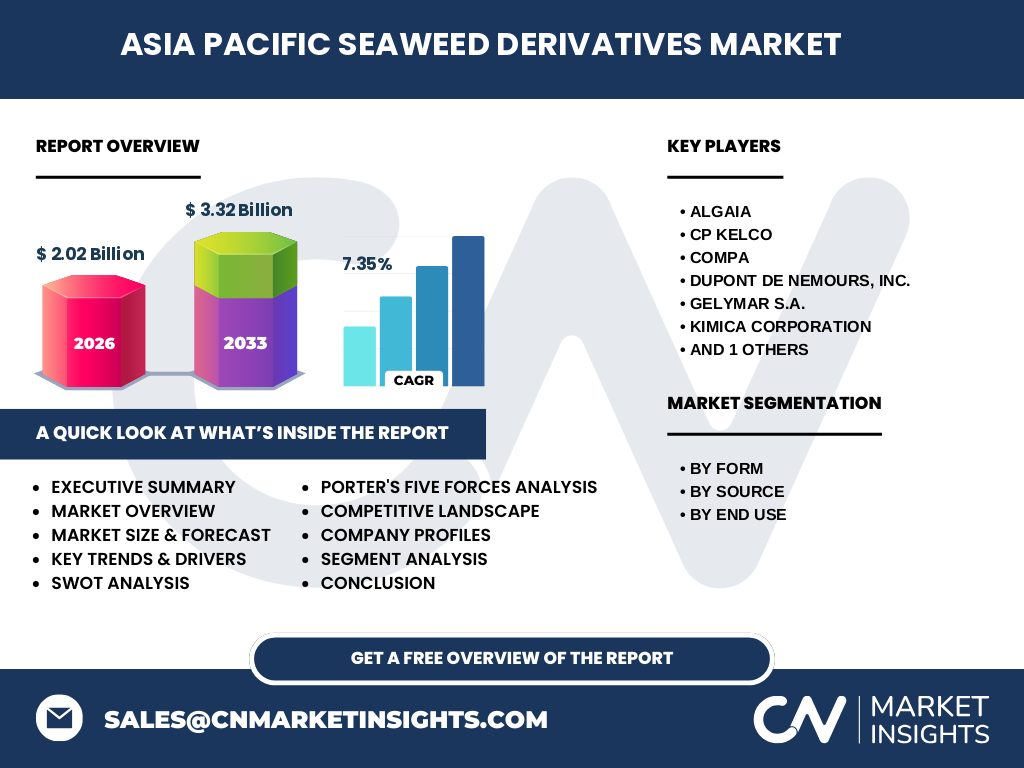

5. Who are the major competitors in the Asia Pacific Seaweed Derivatives Market and what is the level of market consolidation?

Prominent players include Algaia, CP Kelco, Compa, DuPont de Nemours, Inc., Gelymar S.A., KIMICA Corporation, and W Hydrocolloids, Inc. The market shows moderate consolidation, with these firms leveraging strategic partnerships, joint ventures, and acquisitions to expand their product portfolios and geographic reach. Competitive differentiation focuses on advanced extraction techniques, diversified seaweed sourcing, and tailored solutions for specific end‑use applications.

6. What are the high‑level findings presented in the executive summary of the Asia Pacific Seaweed Derivatives Market?

The executive summary highlights a market size of US$2.02 billion in 2026, projected to reach US$3.32 billion by 2033, reflecting a CAGR of 7.35 %. Growth is driven by expanding food‑and‑beverage applications, increasing agricultural adoption of seaweed biofertilizers, and rising pharmaceutical interest in marine bioactives. The region benefits from abundant seaweed resources, supportive policy frameworks, and innovative R&D, positioning it for sustained expansion throughout the forecast horizon.

7. What are the forecast expectations for the Asia Pacific Seaweed Derivatives Market from 2025 to 2032?

Based on the provided CAGR of 7.35 %, the market is expected to maintain steady double‑digit growth, surpassing the US$3 billion mark by the early 2030s. The forecast anticipates balanced expansion across all three form segments—liquid, powder, and flakes—while the source mix will diversify, with brown seaweed derivatives gaining prominence due to their high alginate content. End‑use demand, particularly in food‑and‑beverage and pharmaceutical sectors, will continue to be the primary driver.

8. How is the Asia Pacific Seaweed Derivatives Market sized and shared across its key segments?

Segmentation by form includes liquid, powder, and flakes, each capturing distinct application niches. By source, the market is divided among red, brown, and green seaweed, with brown seaweed traditionally dominant in alginate production. End‑use segmentation covers food and beverages, agricultural products, animal feed additives, and pharmaceuticals. While exact monetary shares are not disclosed, the breadth of segmentation illustrates a diversified market structure that mitigates reliance on any single product type.

9. What is the geographic distribution of the Asia Pacific Seaweed Derivatives Market size and share?

The market is concentrated in coastal economies with strong seaweed cultivation traditions, notably China, Indonesia, the Philippines, Japan, and South Korea. These countries collectively account for the bulk of the US$2.02 billion market in 2026, reflecting their extensive production capacity, established processing facilities, and export orientation. The forecasted growth will be supported by emerging seaweed farming initiatives in Vietnam and Thailand, further broadening the regional footprint.

10. What are the key findings of the regional analysis for the Asia Pacific Seawater Derivatives Market?

China leads in both volume and value, driven by large‑scale integrated farms and advanced hydrocolloid processing. Indonesia and the Philippines excel in brown and red seaweed harvests, feeding global food‑additive supply chains. Japan’s market is distinguished by high‑value pharmaceutical derivatives, while South Korea focuses on innovative functional foods. Regional analysis underscores the importance of localized R&D, government incentives, and infrastructure upgrades to sustain competitive advantage.

11. Which companies are leading the Asia Pacific Seaweed Derivatives Market and what are their strategic approaches?

Algaia emphasizes sustainable sourcing and organic certification, targeting premium food markets. CP Kelco leverages its global hydrocolloid portfolio to cross‑sell seaweed derivatives to existing customers. DuPont integrates seaweed extracts into its nutrition and health platforms, pursuing biotech collaborations. KIMICA Corporation focuses on animal feed additives, investing in high‑throughput extraction. Each leader adopts a mix of product innovation, geographic expansion, and strategic partnerships to capture market share.

12. How does Porter’s Five Forces framework assess the competitive dynamics of the Asia Pacific Seaweed Derivatives Market?

Threat of new entrants is moderate; entry barriers include capital‑intensive processing and stringent food safety standards. Bargaining power of suppliers is relatively low due to abundant seaweed biomass, though premium species can command higher prices. Bargaining power of buyers is moderate, driven by large food manufacturers seeking cost‑effective, functional ingredients. Threat of substitutes exists from synthetic hydrocolloids, yet natural branding reduces substitution risk. Industry rivalry is intense, with several multinational and regional firms competing on quality, price, and innovation.

13. What are the SWOT highlights for the Asia Pacific Seaweed Derivatives Market?

Strengths: Rich natural resource base, growing consumer preference for natural ingredients, and versatile applications. Weaknesses: Variable raw‑material quality and limited high‑tech processing capacity in some locales. Opportunities: Expansion into nutraceuticals, biodegradable materials, and personalized nutrition. Threats: Climate change impacts on seaweed yields and increasing regulatory scrutiny on marine bioproducts.

14. How is the value chain structured for the Asia Pacific Seaweed Derivatives Market?

The value chain begins with seaweed cultivation (wild harvest or aquaculture), followed by collection, primary cleaning, and drying. Extraction and purification processes generate liquid, powder, or flake derivatives, which are then formulated into end‑product applications. Distribution channels include direct B2B supply to food processors, agricultural cooperatives, feed manufacturers, and pharmaceutical firms. Supporting services such as logistics, quality certification, and R&D collaborations complete the chain.

15. What investment insights are crucial for stakeholders considering the Asia Pacific Seawater Derivatives Market?

Investors should prioritize companies with vertically integrated operations that control cultivation through final product formulation, as this reduces supply risk. Funding opportunities exist in advanced extraction technologies, sustainable aquaculture platforms, and niche high‑value pharma extracts. Partnerships with research institutions can accelerate product differentiation, while expanding into emerging markets (e.g., Vietnam) offers growth leverage. Monitoring regulatory developments is essential for risk mitigation.

16. What are the key takeaways from the Asia Pacific Seawater Derivatives Market conclusion?

The market is on a robust growth trajectory, underpinned by a solid base of natural resources, escalating demand for clean‑label ingredients, and expanding application horizons. With a projected market size of US$3.32 billion by 2033 and a healthy CAGR of 7.35 %, the region is poised for sustained expansion. Success will hinge on innovation, supply‑chain resilience, and alignment with sustainability standards.

17. How was the research for the Asia Pacific Seawater Derivatives Market conducted?

The study employed a mixed‑method approach combining primary interviews with industry experts, secondary data extraction from reputable databases, and quantitative modeling to forecast market size. Trend analyses, competitive benchmarking, and scenario planning were integrated to ensure a comprehensive view of market dynamics.

18. What is the scope of the research, including coverage and limitations?

The scope covers the entire Asia Pacific region, all major seaweed sources (red, brown, green), form factors (liquid, powder, flakes), and end‑use applications (food and beverages, agricultural products, animal feed additives, pharmaceuticals). Limitations are limited to publicly available financial figures; proprietary company data were not disclosed.

19. Which key companies have made recent developments in the Asia Pacific Seawater Derivatives Market?

Algaia announced a new organic-certified liquid extract line aimed at the premium beverage sector. CP Kelco launched a high‑viscosity brown‑seaweed powder for plant‑based cheese alternatives. DuPont de Nemours, Inc. entered a joint venture with a Korean biotech firm to develop marine‑derived drug delivery systems. KIMICA Corporation expanded its animal‑feed portfolio with a patented seaweed‑based growth promoter. These activities indicate ongoing product innovation and strategic collaboration across the market.